Another month, another strong retail spending number. The tenacity of the Australian consumer in the face of rising inflation, five interest rate hikes, a precipitous drop in house prices and no real wage growth is becoming something of a riddle.

Elizabeth Knight, The Age, September 28, 2022

There is no riddle, but there are several conflicting drivers and long lags at work. Annual retail sales growth in July and August were at near record highs: 16.5% and 19.2% respectively. Month to month growth over the four months to August was just running at an annualised rate of just under 9%: slower, still very strong.

What many commentators don’t understand is that the impacts of higher interest rates and lower residential property prices operate with long lags. The negative impact of higher interest rates takes up to 18 months to peak and for lower residential property price the lags are up to 12 months.

In the meantime there are currently four positive drivers of retail sales which operate with short lags:

- Households are saving a lower proportion of their income than they did in 2020 and 2021. That means they are currently spending a higher proportion of their income.

- A spike in price inflation means that consumers have to spend more money for the same volume of goods and services – for example fruit and vegetables, meals out, and many other items.

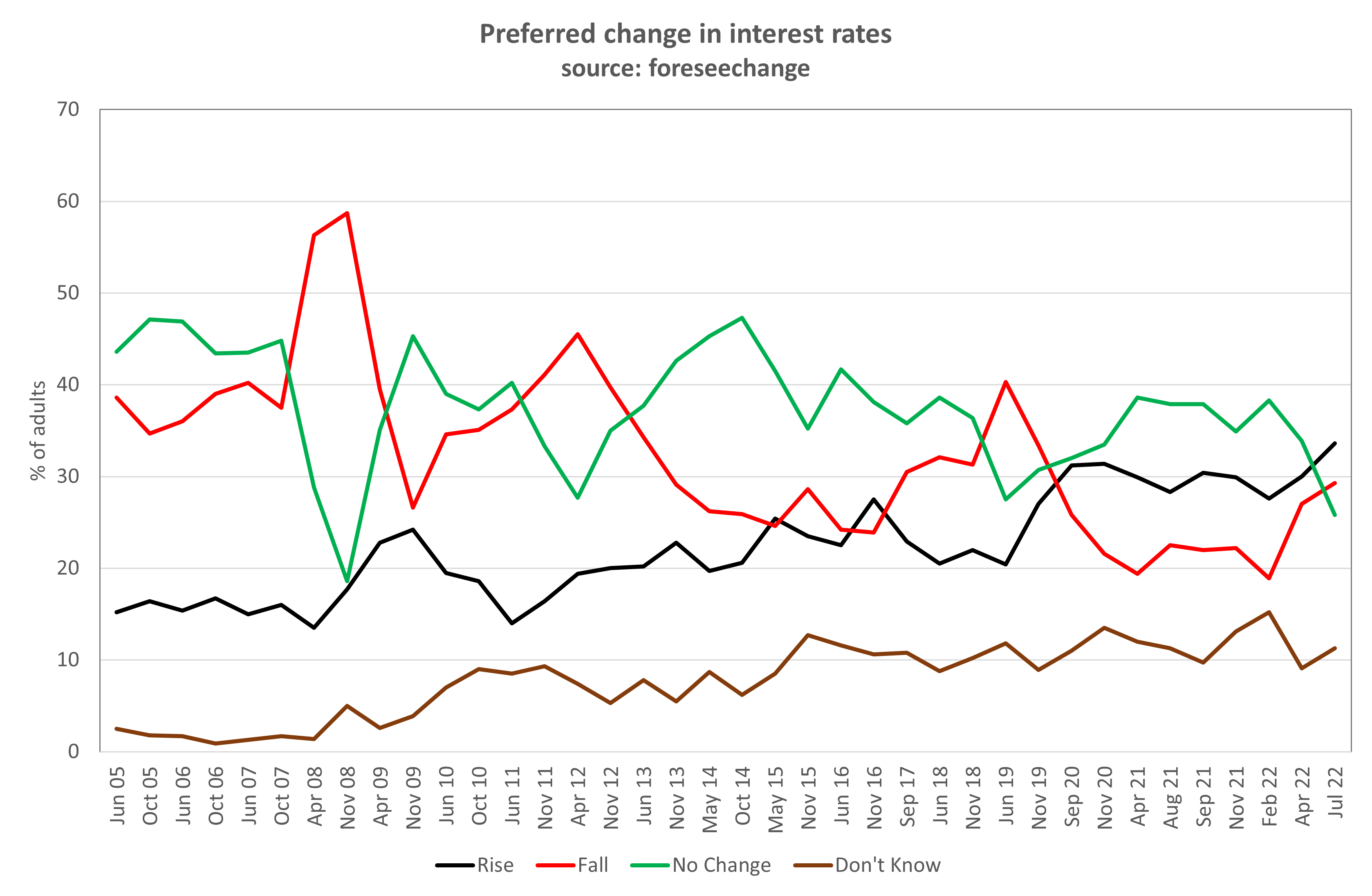

- More people now prefer higher interest rates than lower interest rates. Consumers have increased bank deposits by more than $300 billion since the end of 2019. As interest rates rise, interest income is rising steeply which gives consumers more money to spend – which they do quickly. This is based on tracking surveys conducted by foreseechange, see chart below.

- Many consumers have submitted their 2021-22 tax return and those who have earned less than $126,000 are receiving a low and middle income tax offset of up to $1,500. This boosts disposable income in the short-term and is an example of a monetary and fiscal policy collision – the Reserve Bank is trying to take money away from consumers while the federal government gives them more!

Why the long lags on the negative impact of rising interest rates?

Many households with a mortgage have built up a buffer, especially while interest rates have been at a record low. They have paid more than the minimum amount required on their loans (or kept paying the minimum that was required when interest rates were higher) and some have offset accounts which have been boosted during the period of government income support.

Comparison of household debt and household deposits

In 2008, when interest rates and interest payments were at a record high, the ratio of household debt to household deposits was 2.7. Saving increased from 2010 and in 2021 the ratio of household debt to household deposits was 1.9. Clearly, interest rate sensitivity is now much lower than it was in 2008 – consistent with the interest rate preference chart shown above.

Risks and opportunities for consumer marketers

With strong consumer spending now, which is likely to slow over the next six months, there is a risk that too much stock will be ordered unless the slowdown is anticipated.

Consumers who have savings, and who will increasingly earn more income and spend more, represent an opportunity as spending declines amongst consumers with debt.

Risks for monetary policy

The long lags in the negative reaction of consumer spending in response to higher interest rates, coupled with the initial positive reaction, may mislead the Reserve Bank of Australia into ramping up interest rates more than is needed – with the risk of engineering a significant economic slowdown and possibly a recession.

Outlook for consumer spending

Consumer spending growth is likely to slow over the next year as the impact of the low and middle income tax offset wanes and the negative impact of higher interest rates starts to cut in.

More information and updates

Quarterly updates of our unique consumer tracking data and analysis of consumer spending data will be provided to clients, commencing in late October 2022.

Contact foreseechange for a copy of the report and to subscribe to updates.